Positive Comments: The Monopoly Strategy of Tech Giants Accelerates the Maturity of the Quantum Computing Industry and Promotes Technology Commercialization and Ecosystem Collaboration

The leap of quantum computing from a “theoretical toy” to a “computing powerhouse” would not have been possible without the strategic layouts and resource investments of tech giants. Companies such as NVIDIA, IBM, and Google are propelling technological breakthroughs, scenario implementation, and ecosystem building in the quantum computing industry at an extraordinary pace through their “monopoly + ecosystem” strategies. The positive impacts are mainly reflected in the following three aspects:

I. Accelerating Technology Standardization and Ecosystem Maturity, and Lowering Industry Entry Barriers

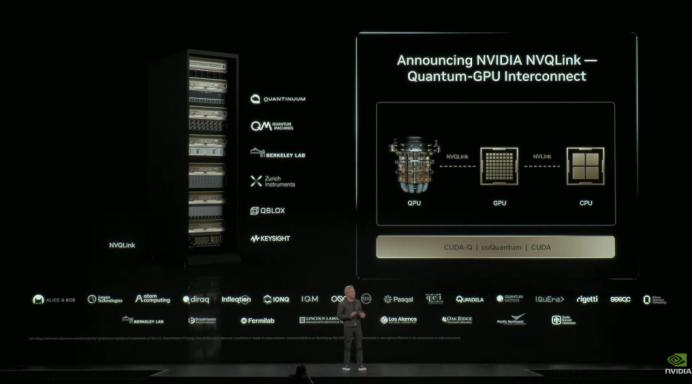

The technological paths of quantum computing are highly fragmented (with five major paths coexisting, including superconducting, photonic, and ion – trap technologies), and there is an urgent need for synergy between hardware and classical computing. NVIDIA’s NVQ Link hybrid computing architecture provides a unified computing operating system for quantum hardware of different technological paths through the in – depth integration of “quantum + GPU”. The core value of this “switchboard operator” role lies in: on the one hand, it solves the problem of quantum computing’s dependence on classical computing power in data pre – processing, error correction, and other stages, increasing the efficiency of quantum computing by 10 times; on the other hand, by integrating 17 quantum enterprises and 9 national laboratories, the NVQ Link ecosystem covers mainstream technological paths, promoting the unification of interface standards and collaboration protocols. This standardization process significantly lowers the technological barriers for small and medium – sized enterprises to access quantum computing, enabling more enterprises to focus on scenario application development rather than underlying architecture construction. For example, commercial cases such as JD.com’s warehousing optimization and the rainfall prediction of the Anhui Meteorological Bureau are typical examples of rapid implementation relying on the hybrid computing ecosystem.

II. Concentrated Investment in Capital and R & D, Accelerating the Transformation of Technology from the Laboratory to the Industry

The R & D of quantum computing requires a long – term and high – investment “money – burning” model. From 2020 to 2025, the global annual R & D investment increased from $1 billion to $5 billion, and the R & D investment of giants such as IBM and Google soared from hundreds of millions of dollars to billions of dollars. This concentrated investment has directly driven rapid breakthroughs in technological indicators: the number of qubits increased from 53 qubits in 2019 (Google’s “Sycamore”) to 176 qubits in 2024 (the whole – machine of Guodun Quantum), and the fidelity increased from less than 99% in the early stage to 99.99% in the ion – trap path. At the same time, the giants’ “three – step monopoly strategy” (short – term equipment and software monopoly, medium – term scenario monopoly, and long – term rule – making) provides a clear commercialization path for technology transformation. For example, NVIDIA uses the cuQuantum software to simulate quantum circuits and cooperates with OpenAI to optimize the stability of qubits, transferring its AI technology accumulation to the quantum field; IBM’s annual – fee model for the enterprise version of Qiskit (with an expected revenue of $1.2 billion in 2026) provides a viable profit model for software serviceization. This closed – loop of “R & D – commercialization – reinvestment” significantly shortens the transformation cycle of quantum computing from the laboratory to the industry.

III. Scenario Verification and Ecosystem Collaboration, Activating the Practical Value of Quantum Computing

The real significance of quantum computing lies in solving complex problems that classical computing cannot handle. Currently, the implementation of scenarios such as logistics (JD.com reduced costs by 15%), meteorology (an 8% increase in rainfall prediction accuracy), medicine (a 40% reduction in the new drug R & D cycle), and finance (a three – fold increase in option pricing speed) has initially verified the practical value of quantum computing. The giants further amplify this value by integrating the resources of hardware, software, and scenario providers through ecosystem alliances. For example, NVIDIA is collaborating with Dow Chemical to develop a quantum material simulation platform, aiming to capture 60% of the global high – end material R & D computing power market; the quantum encryption communication system jointly developed by IBM and JPMorgan Chase plans to charge an annual “protection fee” equivalent to 0.3% of the global banks’ annual revenue. The large – scale application of these scenarios not only brings stable revenue to the giants but also attracts the attention of more industry users (such as those in the energy and aviation sectors), promoting the transition of quantum computing from “technology verification” to “value creation”.

Negative Comments: The Monopoly Strategy Implies the Risk of Technology Lock – in, Potentially Inhibiting Industry Diversity and Fair Competition

Although the giants’ monopoly strategy has accelerated the maturity of the quantum computing industry, their centralized control over technological standards, scenario resources, and rule – making power has also brought about potential problems that cannot be ignored, which may have a negative impact on the long – term healthy development of the industry.

I. The Risk of Single – Track Technology, Inhibiting the Innovation Vitality of Diverse Technological Paths

The technological paths of quantum computing are still in a stage of “a hundred schools of thought contending”. Each path, such as superconducting, photonic, and ion – trap, has its own advantages and disadvantages (for example, photonic technology can operate at room temperature but is difficult to scale up in terms of the number of qubits, while ion – trap technology has high fidelity but is expensive). However, NVIDIA’s NVQ Link ecosystem, by integrating 17 major quantum enterprises, actually centralizes the dominance of technology collaboration under the hybrid computing architecture. This “self – centered” ecosystem building model may lead to the marginalization of other technological paths (such as the slower – progressing silicon semiconductor path) due to the lack of ecosystem support. For example, Intel’s silicon semiconductor path, which has the advantage of being compatible with existing chip production lines, could have been a key path to reducing the cost of quantum computing. However, since it is not included in the NVQ Link ecosystem, its R & D resources and commercialization opportunities may be further compressed. In the long run, the industry may miss the opportunity to explore better solutions due to the single – track technology.

II. Increased Market Concentration, Squeezing the Survival Space of Small and Medium – Sized Enterprises

The giants’ “three – step monopoly strategy” essentially controls the key links of the industrial chain: in the short term, they reap dividends through equipment (such as a $200,000/unit authorization fee for the NVQ Link interface) and software (such as a $100,000/household annual fee for Qiskit); in the medium term, they build barriers through high – value scenarios (financial security, AI training); in the long term, they control the rules through standard – setting (17 international standards). This full – chain control from hardware to software, from scenarios to rules will lead to the concentration of market share in a few giants. For example, it is estimated that by 2028, hardware and software related to hybrid computing will account for more than 70% of the quantum computing market, and NVIDIA’s share of quantum business revenue will increase from 8% to 15%; by 2030, the annual revenue of IBM’s enterprise version of Qiskit is expected to exceed $3 billion, and the scale of NVIDIA’s hybrid computing ecosystem will reach $50 billion. If small and medium – sized enterprises want to participate in the quantum computing industry, they either have to pay high authorization fees to access the giants’ ecosystems or be excluded due to high technological barriers, which will seriously inhibit the innovation vitality and fair competition in the industry.

III. Technology Lock – in and Pricing Power Monopoly, Potentially Driving up the Overall Industry Cost

The technological barriers formed by the giants through ecosystem alliances and standard – setting may lead to the “technology lock – in” effect. Once users choose an ecosystem (such as NVQ Link), their subsequent upgrades and maintenance will be highly dependent on the products and services of that ecosystem. For example, if an enterprise using NVIDIA’s hybrid computing architecture wants to switch to other quantum hardware (such as the photonic path), it may need to re – develop interfaces and software at a very high cost. This lock – in effect will strengthen the giants’ pricing power, thereby driving up the overall industry cost. Take IBM’s quantum encryption communication system as an example. It plans to charge banks an annual “protection fee” equivalent to 0.3% of their annual revenue. This pricing model based on monopoly power may far exceed the actual service cost and ultimately be passed on to downstream users (such as ordinary consumers). In addition, in the long run, the giants’ monopoly of the supercomputing market (such as IBM’s goal of occupying 75% of the market share) may lead to high computing power prices, inhibiting the popularization of quantum computing in a wider range of fields.

Advice for Entrepreneurs: Focus on Differentiated Innovation and Find “Niche Opportunities” in the Giants’ Ecosystems

Facing the giants’ monopoly strategy, entrepreneurs should avoid direct competition with the giants and instead focus on “niche opportunities” in segmented scenarios, differentiated technological paths, and ecosystem collaboration. They can start from the following directions:

I. Deeply Explore Vertical Scenarios and Develop Customized Quantum Applications

The giants’ monopoly focuses on general scenarios (such as finance and medicine) and high – value fields (such as AI training and material R & D), while there are still a large number of unmet needs in segmented scenarios such as agriculture, environmental protection, and personalized medicine. Entrepreneurs can develop customized solutions based on quantum algorithms for specific problems in these scenarios (such as optimizing the cold – chain logistics path of agricultural products, simulating pollutant diffusion, and screening cancer – targeting drug molecules). For example, for agricultural meteorological prediction, quantum computing can be used to optimize the crop irrigation model to improve water resource utilization efficiency; for the environmental protection field, a quantum simulation platform can be developed to predict the diffusion path of industrial pollution to assist in policy – making. The needs in these segmented scenarios are more specific, the competition is smaller, and the commercial value can be quickly verified through actual results.

II. Pay Attention to Differentiated Technological Paths and Form Technological Features

Currently, the five major technological paths of quantum computing each have their own advantages and disadvantages. The giants’ ecosystem layouts mainly cover mainstream paths (such as superconducting and photonic), while slower – progressing but high – potential paths (such as silicon semiconductor and neutral atoms) may become breakthrough points for entrepreneurs. For example, the silicon semiconductor path is compatible with existing chip production lines. If breakthroughs can be made in qubit number expansion or fidelity improvement, it may significantly reduce the hardware cost of quantum computing; the neutral atom path has low cost and is suitable for cost – sensitive scenarios such as education and scientific research. Entrepreneurs can choose one technological path and focus on single – point breakthroughs (such as increasing the coherence time of silicon qubits or optimizing the laser control accuracy of neutral atoms) to form differentiated technological barriers and avoid direct conflict with the giants’ “full – path coverage” strategy.

III. Utilize the Giants’ Ecosystems while Maintaining Technological Independence

The giants’ hybrid computing ecosystems (such as NVQ Link) provide entrepreneurs with opportunities to access quantum computing power at low cost, but they should avoid over – dependence on a single ecosystem. It is recommended that entrepreneurs retain the independent R & D ability of core algorithms and application layers while using the giants’ hardware interfaces and software tools (such as cuQuantum). For example, when developing a logistics optimization application, quantum computing power support can be obtained based on NVQ Link, but the core logic of the path optimization algorithm should be kept in their own hands to avoid technological discontinuity due to ecosystem switching (such as the emergence of a better hybrid computing architecture in the future). In addition, multiple ecosystems (such as IBM’s Qiskit and Google’s Quantum Cloud) can be accessed simultaneously to reduce the risk of technology lock – in.

IV. Plan for Long – Term Scenarios in Advance and Participate in Industry – University – Research Collaboration

The long – term value of quantum computing (such as quantum universe simulation and the replacement of supercomputers by general – purpose quantum machines) requires early technological reserves. Entrepreneurs can cooperate with universities and national laboratories (such as the U.S. Department of Energy laboratories mentioned in the news) to participate in cutting – edge research projects (such as quantum error – correcting codes and high – fidelity qubit control) and accumulate patents and technological achievements. For example, they can cooperate with domestic quantum computing laboratories to develop quantum material simulation algorithms to prepare for future new – energy battery R & D scenarios; or participate in the formulation of quantum security communication standards to enhance their voice in industry rules. This “pre – research + cooperation” model can not only reduce R & D costs but also accumulate technological advantages for long – term competition.

V. Pay Attention to the Standardization Process and Promote Open Collaboration

Entrepreneurs should actively participate in the standard – setting work of industry associations and alliances to promote the openness and compatibility of key standards such as interfaces and security. For example, regarding the interface standards between quantum computing and classical computing, small and medium – sized enterprises can jointly propose more flexible and low – threshold protocol solutions to avoid being “locked in” by the giants’ private standards; in the field of security standards, they can promote the transparent pricing of “quantum security suites” to prevent the giants from using their monopoly power to raise fees. Through collective voices, entrepreneurs can balance the giants’ standard – setting power to some extent and strive for space for the diversified development of the industry.

The debate between “monopoly” and “innovation” in quantum computing is essentially a game between the accelerated implementation of technology and the balance of the industry ecosystem. The giants’ strategies have promoted the maturity of the industry, but the differentiated innovation of entrepreneurs can truly activate the full – scenario value of quantum computing. Only by finding a balance between “concentrating resources for breakthroughs” and “diversified exploration and innovation” can quantum computing transform from “the giants’ business” into “an opportunity for the entire industry”.

- Startup Commentary”Three post-2005 entrepreneurs are reported to have secured a new financing of 350 million yuan.”

- Startup Commentary”Retired and Reemployed: I Became Everyone’s “Shared Grandma””

- Startup Commentary”YuJian XiaoMian Breaks Issue Price on Listing: Where Lies the Difficulty for Chinese Noodle Restaurants to Break Through in the Market? “

- Startup Commentary”Adjusting Permissions of Doubao Mobile Assistant: AI Phones Are a Flood, but Not a Beast”

- Startup Commentary”Moutai’s Self – rescue and Long – term Concerns”